Singapore Corporate Bank Account Closed? Why It Happens & How to Prevent It (2026 Guide)

In the last 12 months, we have seen a disturbing trend: legitimate, profitable Singapore companies receiving a “30-Day Closure Notice” from their banks.

No explanation. No appeal process. Just a letter stating that the bank can “no longer support your banking relationship.”

If this happens, your business effectively stops. You cannot pay staff, you cannot receive client funds, and opening a new account becomes nearly impossible once you are “offboarded” by a major local bank (DBS, OCBC, UOB).

This is not bad luck. It is compliance failure.

In 2026, Singapore banks are no longer just looking at your initial application. They are using AI-driven continuous monitoring to scan your transactions for Anti-Money Laundering (AML) risks. If your paperwork doesn’t match your money flow, you are flagged.

Here is why accounts get closed and how you can protect your business.

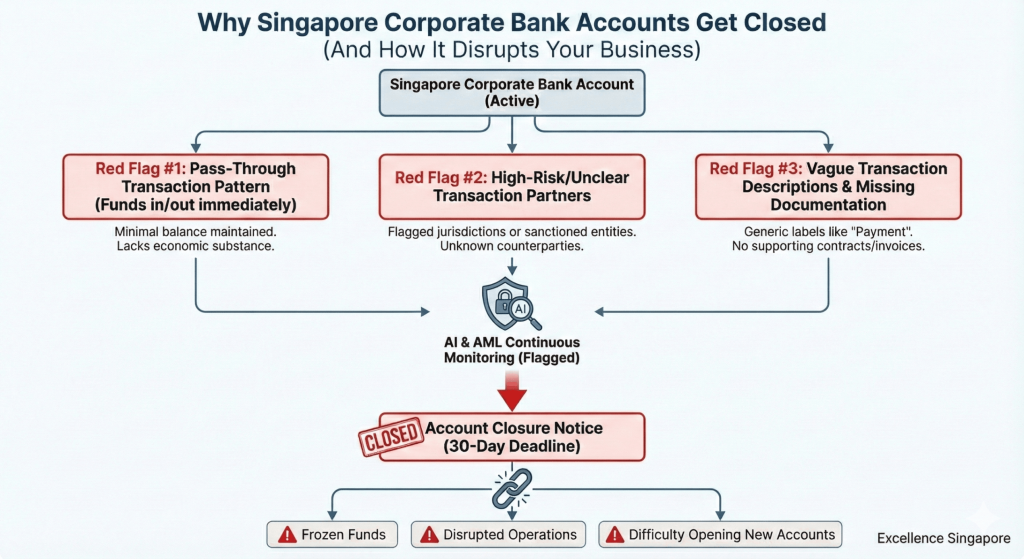

The “Silent Killer”: Periodic Reviews

Most business owners believe that once the bank account is open, the hard work is done. This is dangerous thinking.

Banks conduct Periodic Reviews (annually or semi-annually). They compare your actual transaction patterns against the “Business Profile” you declared when you opened the account.

If you told the bank you are a “Marketing Agency” with a turnover of S

Red Flag #1: The “Pass-Through” Trap

This is the most common reason for immediate closure.

A “Pass-Through” account is one where money comes in and immediately goes out, leaving a minimal balance. To a bank’s compliance team, this looks like money laundering or “layering.”

The Scenario: You receive $50,000 from Client A. Within 24 hours, you transfer $49,500 to Supplier B overseas. The Bank’s View: “This company has no economic substance. It is just a shell moving money.”

The Fix: You must maintain a healthy average daily balance. More importantly, you need Contractual Proof. Every major outflow must be backed by an agreement or invoice. If the bank asks “What is this payment?”, and you cannot produce a contract within 48 hours, you are at risk.

Need robust agreements to justify your transactions? Our Contract and Agreement Templates ensure your paper trail is audit-ready.

Red Flag #2: Transacting with “High-Risk” Parties

You might be clean, but are your clients?

If you receive funds from a company that has been flagged for sanctions evasion or fraud, that “taint” transfers to you. This is common in sectors like commodities trading, crypto, or cross-border consulting.

Furthermore, if you are a foreign-owned company using a “Sleeping” Nominee Director who has no idea what your business does, banks view this as a massive risk. They want to see that the local director is competent and involved.

Ensure your leadership passes the “sniff test.” Our Nominee Director Services provide credible, compliant local representation, not just a signature.

Red Flag #3: The “Description” Mismatch

When you transfer money, do you write “Loan” or “Payment” in the reference field?

Vague payment descriptions are a trigger for AML algorithms.

- Bad: “Consulting fees”

- Good: “Inv-2026-001: SEO Services for Q1”

Banks need to trace the nature of the trade. If your transaction descriptions are consistently vague, you will be flagged for a manual review. If that review finds gaps in your Company Secretary records (e.g., missing Board Resolutions for large loans), the account is closed.

How to “Audit-Proof” Your Bank Account

You cannot stop the banks from checking you, but you can survive the check.

- Maintain Your “Defense File”: For every transaction over S$10,000, have the Invoice and the Contract saved in a dedicated folder.

- Update Your Business Profile: If your business pivots (e.g., from Web Design to E-Commerce), inform the bank before they see strange transactions.

- Local Substance: Use a registered office that handles mail properly and a local secretary who keeps your ACRA profile pristine.

Conclusion: Compliance is Your Life Jacket

A bank account is a privilege, not a right. In Singapore’s strict regulatory environment, the bank’s risk appetite is low. They would rather close 10 innocent accounts than let one money launderer slip through.

Don’t give them a reason to doubt you.

Is your paperwork messy? We don’t just file forms; we help structure your compliance so your business stays open.

Contact Excellence Singapore Today regarding our Due Diligence and Corporate Secretarial services.