My Singapore Business Bank Account Was Rejected: What Now? (The 5 Hidden Reasons & Appeal Guide)

In 2025 and 2026, the hardest part of starting a business in Singapore isn’t the incorporation—it’s the Bank Account Opening.

We are seeing a surge in foreign founders who receive a short, vague “Regret Letter” from traditional banks like DBS, OCBC, or UOB. Because banks are not legally required to disclose the exact reason for a rejection, many founders find themselves in a loop of failed applications.

If you’ve been rejected, it’s likely due to one of the following “hidden” factors that go beyond simple paperwork.

1. The 5 “Hidden” Reasons for Bank Rejection

-

Lack of “Economic Substance”: Banks now verify that your company is a “real” enterprise. If you have no local employees, no physical lease (using only a virtual office), and no Singapore-based clients, the bank may flag you as a shell company risk.

-

Unclear “Source of Wealth” (SoW): As of June 2025, MAS explicitly requires banks to assess your Source of Wealth—the background and legitimacy of how you accumulated your entire net worth over your lifetime—not just the Source of Funds (the specific deposit).

-

High-Risk SSIC Codes: Certain business activities, such as cryptocurrency, precious stones, or vague “General Wholesale Trade,” trigger enhanced due diligence that many retail banking departments are simply not equipped to handle.

-

UBO Complexity: If your company is owned by another offshore entity (e.g., a BVI or Cayman company), the “layers” make it difficult and expensive for banks to verify the Ultimate Beneficial Owner (UBO).

-

Inconsistent Digital Presence: Banks now algorithmically cross-check your LinkedIn profile, company website, and even adverse media. If your online professional history doesn’t match your business activity, it is flagged as a fraud risk.

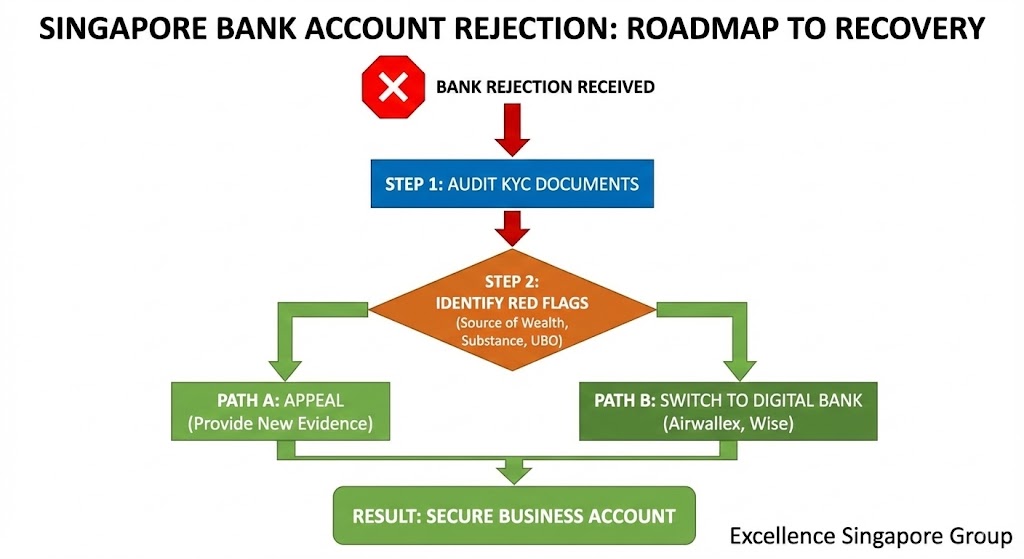

2. The “Recovery Roadmap”: Your 4-Step Plan

If you have already received a rejection, do not simply apply to another bank tomorrow. Instead, follow this roadmap:

-

Step 1: Document Audit: Review your KYC pack. Are your CVs, business plans, and proof of address 100% consistent across every document?

-

Step 2: Identify Red Flags: Work with a specialist to find where your “Source of Wealth” narrative might be weak or where your “Economic Substance” is lacking.

-

Step 3: Choose the Path: Determine if you should submit a formal Appeal (only if you have new evidence, like a signed local contract) or Switch to a digital-first provider.

-

Step 4: Secure the Account: Execute your new application with professional representation to ensure no further “black marks” on your record.

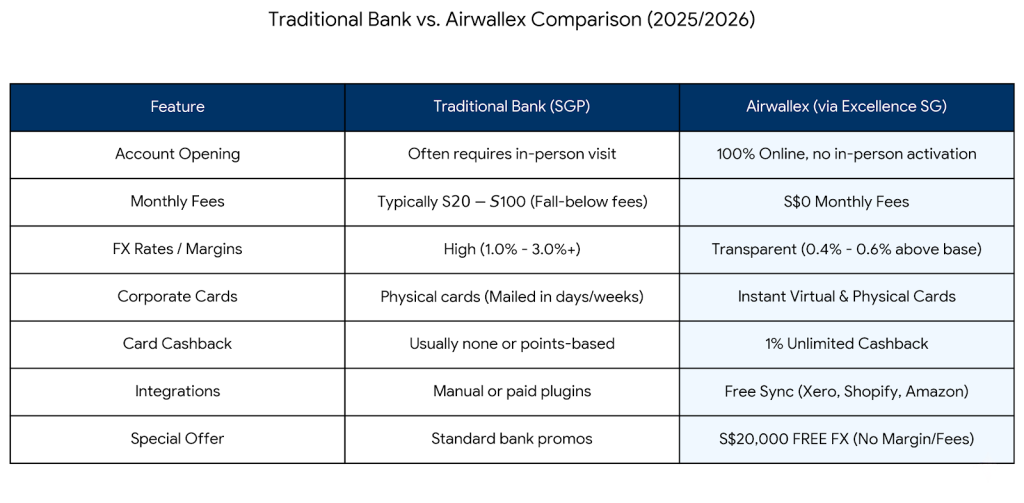

3. The Digital Alternative: Why Startups are Choosing Airwallex

If traditional banks are taking too long (often 4–8 weeks for foreigners) or have rejected your application, Airwallex offers a high-performance alternative designed for modern SMEs.

-

100% Digital Onboarding: Open multiple foreign currency accounts instantly with no in-person activation required.

-

Zero Maintenance Costs: Enjoy S$0 monthly fees and no “fall-below” penalties.

-

Global Reach: Get local bank details for 60+ countries and pay like a local.

-

Unlimited Rewards: Get 1% unlimited cashback on virtual and physical corporate cards.

🎁 Exclusive Excellence Singapore Offer: Sign up for an Airwallex account via our

and enjoy $0 fees and 0% margin on your first SGD $20,000 in FX conversions. Partner Link

Conclusion: Exit the Rejection Loop

A bank rejection is a speed bump, not a dead end. By identifying the hidden reason for your “Regret Letter” and pivoting to a digital-first strategy, you can get your business operational in days rather than months.

Ready to secure your business account? Contact Excellence Singapore Group for a Banking Consultation